Buy Refurbish Refinance Rent (BRRRR): Complete UK Strategy Guide 2026

Buy Refurbish Refinance Rent (BRRR / BRRRR) is a UK property investing strategy where you buy a discounted property in cash or with a bridging loan, refurbish it to add value, refinance at the new higher value to pull most or all of your capital out, then rent it for cashflow. Done well, you recycle your deposit indefinitely and build a portfolio with little or no fresh capital after the first deal.

For a focused look, see our piece on flipping houses in the UK — realistic profits and tax.

For the longer comparison, see our piece on buy-to-let or stocks — leveraged returns honestly compared.

The maths is brutal but consistent: you need to buy at 70–75% of the post-refurb value (PRV), do a refurb that adds at least 1.3x its cost in value, and refinance at 75% LTV. Get any of those three wrong and you can’t recycle your capital.

- What BRRRR (Buy Refurbish Refinance Rent) actually is

- The BRRRR maths — why it works (and when it doesn’t)

- BRRRR vs standard buy-to-let

- The 7-step BRRRR process

- Financing the buy and the refinance

- The refurbish stage — what adds value, what doesn’t

- Best UK cities for BRRRR in 2026

- Worked example: £140k Stoke terrace, full numbers

- 7 BRRRR mistakes that cost investors their capital

- BRRRR deal scorecard — score before you offer

- Tax: Section 24, Ltd Co, allowable expenses

- FAQs

- BRRRR glossary

Watch: James Nicholson on the BRRRR strategy — when it works, when it doesn’t.

BRRRR is the strategy that built most of my portfolio and the strategy I recommend most often to UK landlords who want to scale beyond 2 or 3 properties. It’s also the strategy investors get wrong most often because they treat it like a standard buy-to-let with extra steps. It isn’t. Each stage has its own discipline, and skipping any of them turns BRRRR into a way of losing money slowly.

This guide is the version of the BRRRR explanation I give in our community when someone asks “how do you actually scale a UK property portfolio?” — covering every stage from sourcing the right discounted property to refinancing without falling foul of the 6-month rule, plus the seven mistakes I see weekly that cost investors their entire deposit.

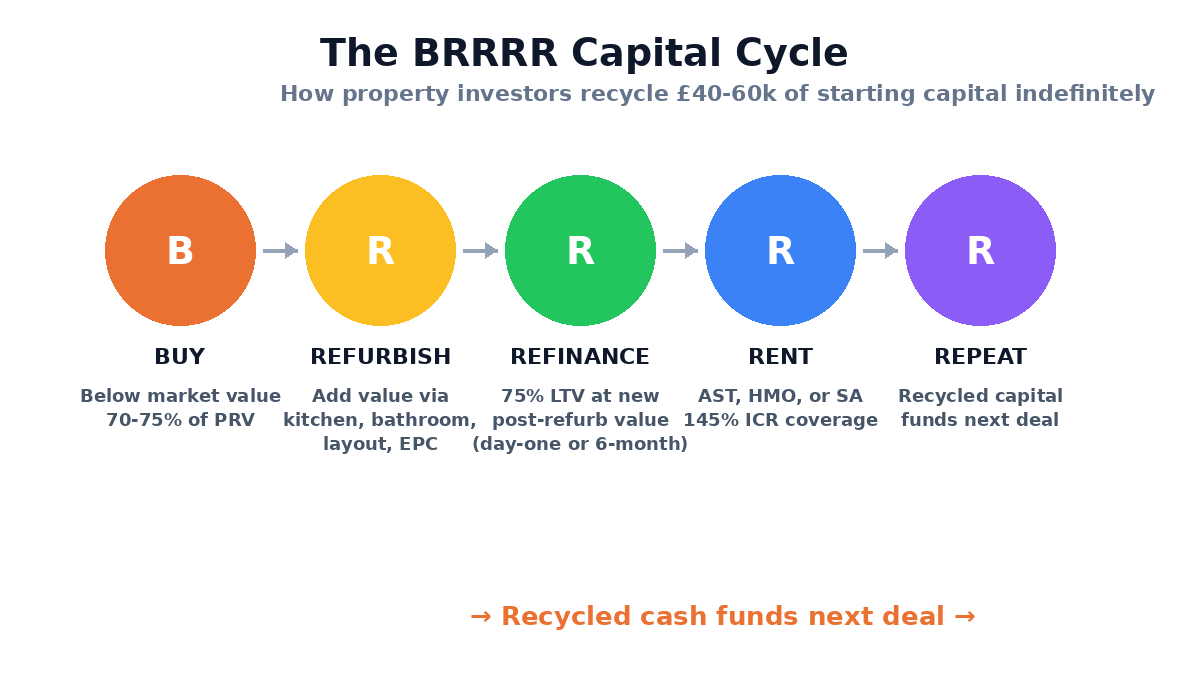

What BRRRR (Buy Refurbish Refinance Rent) actually is

BRRRR — sometimes spelled BRR or BRRR depending on which letters you choose — is a property investing strategy that recycles capital. The full sequence is:

- Buy a property below market value, usually one needing work (probate sales, repossessions, distressed sellers, run-down stock, off-market deals).

- Refurbish it — the work needs to add more value than it costs. Kitchens, bathrooms, layout reconfigurations, EPC improvements, sometimes loft conversions or extensions.

- Refinance at the new (higher) post-refurb value, typically at 75% LTV, pulling most or all of your original deposit back out.

- Rent the finished property to a tenant — single AST, HMO, or serviced accommodation, depending on the area and your strategy.

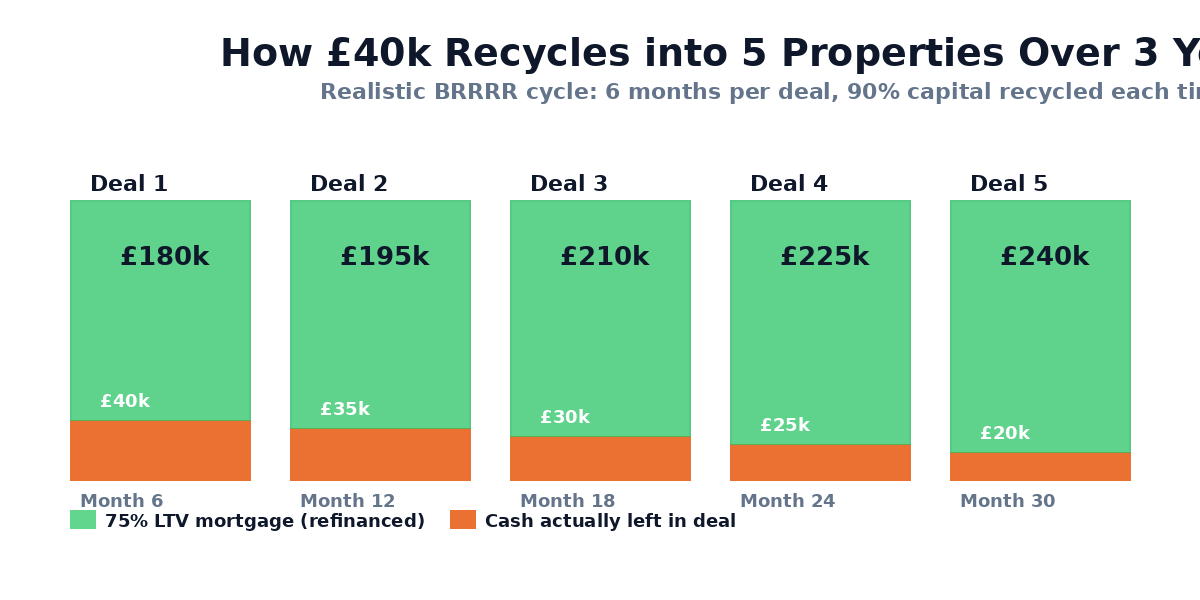

The fifth R — “Repeat” — is implicit. Once your capital is recycled, you do it again. Investors I’ve worked with have built portfolios of 15–30 properties over 5–7 years using BRRRR with as little as £40,000 of starting capital, by recycling it through deals where each refurb pulled the money back out.

The acronym creep is just stylistic. BRR = Buy/Refurbish/Refinance (no rent — implied). BRRR = Buy/Refurbish/Refinance/Rent. BRRRR = Buy/Refurbish/Rent/Refinance/Repeat (re-orders to put rent before refinance). Same strategy, different number of letters. UK investors most commonly use BRR or BRRR; American investors popularised BRRRR. I’ll use them interchangeably here.

The BRRRR cycle: each stage feeds the next, recycling capital indefinitely.

The BRRRR maths — why it works (and when it doesn’t)

The strategy lives or dies on three numbers:

1. The buy price as a percentage of the post-refurb value (PRV). You need to buy at 70–75% of what the property will be worth after refurb. Buy at 80%+ and the refinance won’t release enough to pull your capital out.

2. The refurb’s value-add ratio. Every £1 spent on refurb needs to add at least £1.30 to the property value. Some works add 2x or 3x (loft conversions in the right area, kitchen/bathroom in tired stock); some add nothing or less than they cost (luxury finishes in budget areas, oversized extensions).

3. The refinance LTV and rate. 75% is standard. The rental income then needs to cover the new mortgage at 145% ICR (interest cover ratio) or the lender won’t approve the loan size you need.

Get all three right and you pull 90–110% of your original cash back out. Get one wrong and you leave £15–30k stuck in the deal. Get two wrong and you’ve trapped your deposit. This is why BRRRR isn’t passive — every deal needs deliberate underwriting before you offer.

“Get the buy price wrong and the deal is dead before you start. There’s no recovering a 90%-of-PRV purchase with refurb genius.”

— from a 2025 case where the investor paid £165k on a £180k PRV property and ended up trapping £58k

BRRRR vs standard buy-to-let

Both strategies end with a tenanted property earning monthly cashflow. They differ on capital efficiency and effort.

BRRRR isn’t always better than standard BTL — it’s a tool for a specific situation. If you have £200k of capital and want hands-off rental income, vanilla BTL is the right answer. If you have £40–60k and want to build a portfolio fast, BRRRR is the only viable path.

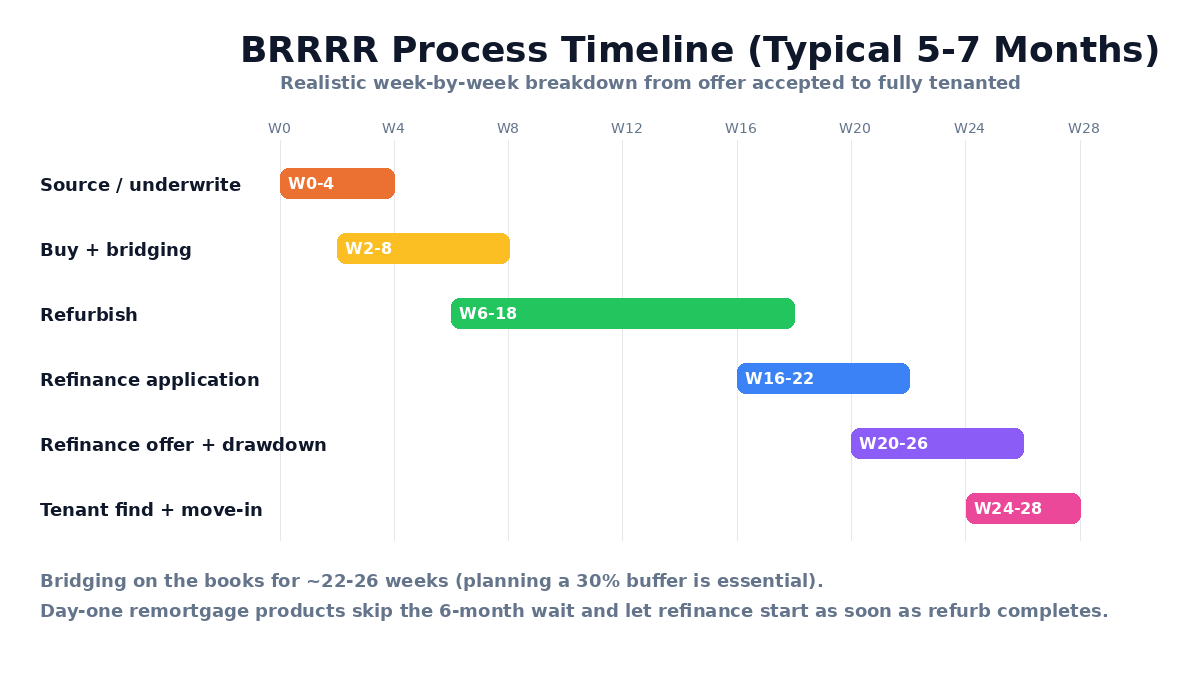

The 7-step BRRRR process

Each stage has its own decisions, costs, and traps. Here’s the sequence and the time each takes in practice:

Step 1 — Source the right property (3–8 weeks)

The deal is everything. You need a property below market value where the work needed will add more than it costs. Sources: estate agent off-market lists, auctions (in person and online), probate sales, repossessions, direct-to-vendor mailing, sourcing companies, private deals from the property community. Avoid Rightmove deals priced near market — they don’t have enough margin for BRRRR maths to work.

Step 2 — Underwrite the deal (1–2 days)

Before you offer, work out: What’s the post-refurb value (PRV)? Get 3 comparable sold prices on the same street. What’s the refurb cost? Walk through with your contractor or use £400–£600/m² as a base for a basic refresh. Will the maths work at 70% of PRV? If not, walk away. There are always more deals.

Step 3 — Buy with bridging or cash (4–8 weeks)

Standard BTL mortgages typically won’t lend on properties needing major work. Use bridging finance (0.65–1% per month, 70–75% LTV on purchase price) or cash if you have it. Some specialist BTL lenders will accept “habitable but tired” properties without bridging — Foundation, Kent Reliance, Precise have refurb-to-let products for these cases.

Step 4 — Refurbish (6–16 weeks)

Project-manage the works to budget and timeline. The schedule should be set when you exchange — Week 1: strip out, Week 3: first fix electrics, Week 5: kitchen install, Week 8: snagging. Cost overruns of 10–20% are normal; budget for them.

Step 5 — Refinance to a term mortgage (4–6 weeks)

Once the property is finished and habitable, refinance to a standard buy-to-let or specialist BTL term mortgage at 75% LTV based on the new post-refurb value. Most lenders apply a “6-month rule” — they won’t lend at the new value until you’ve owned the property for 6 months. Specialist lenders (Foundation, Kent Reliance, Precise) offer day-one remortgage products that ignore the 6-month rule. See my HMO mortgage guide if the property will be operated as a licensable HMO.

Step 6 — Find tenants and let (2–6 weeks)

List with letting agents for AST. If you’re operating as HMO, market each room individually on SpareRoom, Rightmove, OpenRent. Run referencing, draft tenancy agreement, take deposit and first month’s rent.

Step 7 — Repeat (immediately)

The total cycle from buy to refinance to fully tenanted: typically 5–7 months. Once your refinance has cleared and the cash is back in your bank, you start sourcing the next deal.

Realistic timeline: 26-28 weeks (~6 months) from sourcing to fully tenanted, with stages overlapping where possible.

Financing the buy and the refinance

BRRRR financing has two distinct stages. Most deals use different products for each.

Stage 1 — The buy. Three options:

- Cash. Fastest at auction (28-day completion). Cleanest. Requires the full purchase amount in cash, which most investors don’t have.

- Bridging loan. Short-term (3–18 months) finance at 0.65–1% per month. Lenders: Together, MFS, Octopus, Hope Capital, Precise. Up to 75% LTV on purchase price. Best for properties needing work that won’t qualify for term mortgage.

- Refurb-to-let / specialist BTL. Some specialist lenders accept tired properties and roll the refurb into the mortgage. Foundation, Kent Reliance, Precise offer these. Slower than bridging (8–12 weeks vs 4–6) but you skip the bridge-to-term refinance step.

Stage 2 — The refinance. Term mortgage products:

- Standard BTL (mainstream lenders) — 75% LTV, rates 4.5–5.5% as of April 2026. Most apply the 6-month rule.

- Specialist BTL with day-one remortgage — Foundation, Kent Reliance, Precise. 75% LTV, slightly higher rates (5.0–5.8%) but no 6-month wait.

- HMO mortgage if operating as licensed HMO — see my HMO mortgage guide.

- SA mortgage if operating as serviced accommodation — see my SA mortgage guide.

For most BRRRR deals, the cleanest financing path is bridging-then-refinance with a specialist day-one lender on the term side. Total finance cost on a £150k bridge for 6 months at 0.85% pcm is ~£7,650 plus arrangement fees of ~£3,000 — call it £11k of finance cost across the cycle. This needs to be in your underwriting.

Bridging vs refurb-to-let lender comparison

Decision rule of thumb: if the property needs more than 4 weeks of work or won’t be habitable on day one, use bridging. Otherwise, refurb-to-let mortgages save you the bridge-to-term refinance step.

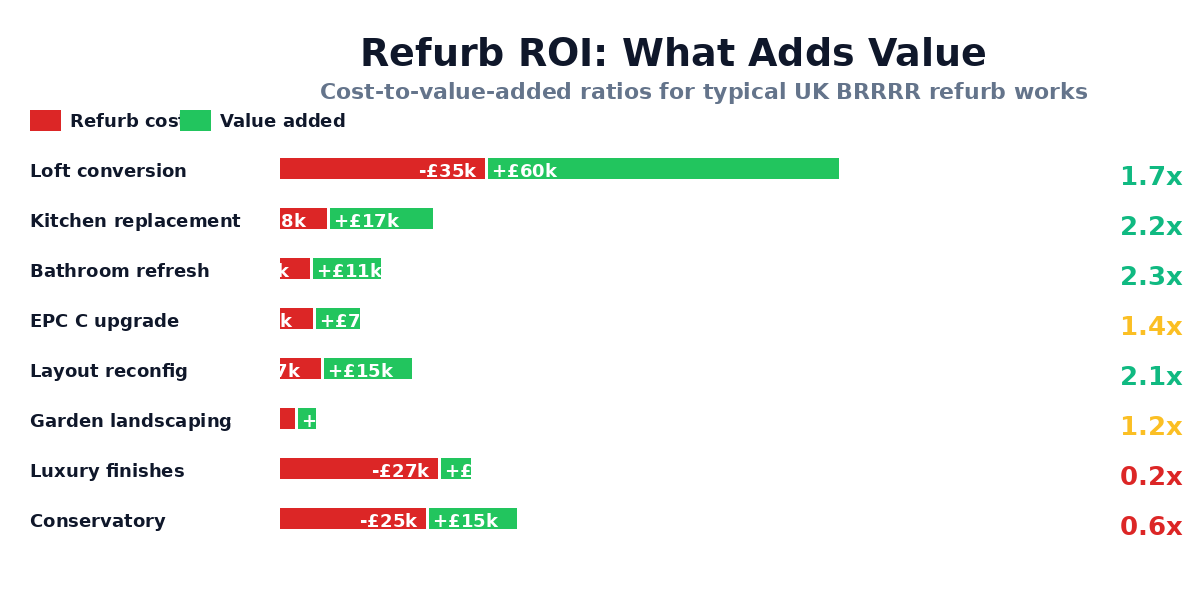

The refurbish stage — what adds value, what doesn’t

Refurbishment is where most BRRRR maths fall apart. Investors over-spec finishes and under-budget time. Here’s what actually adds value vs what doesn’t.

The high-ROI works share a pattern: they fix structural deficiencies in tired stock (no kitchen, no bathroom, poor insulation, awkward layout). The low-ROI works are aesthetic upgrades on already-functional spaces — guests-pleasers that don’t translate to valuer numbers.

Visual ROI comparison: not all refurb works pay back equally. Loft conversions, kitchens and bathrooms lead; luxury finishes and conservatories often lose money.

Best UK cities for BRRRR in 2026

BRRRR works best in markets with three characteristics: tired stock available below market value, healthy rental demand, and recovering or growing house prices. Some cities tick all three; others tick none.

- Liverpool, Bradford, Stoke-on-Trent. Cheap entry (£70–120k), strong yields (7–10%), plenty of tired stock from inherited estates. Best for first-time BRRRR.

- Sheffield, Nottingham, Leicester. Mid-cost (£120–200k), solid yields (6–8%), large student/young professional rental pools. Watch for HMO Article 4 zones.

- Manchester, Leeds, Birmingham (outer wards). Higher entry (£150–250k), modest yields (5–7%), but capital growth tailwinds. BRRRR works on tired terraced stock in commuter wards.

- Newcastle, Sunderland, Middlesbrough. Cheap (£60–110k) but mixed yields and slower capital growth — selective approach needed.

- Northern Ireland (Belfast). Underrated; cheap stock, strong yields, growing market. Less competition from London-based BRRRR investors.

Avoid: London zones 1–4 (cap rates too tight for BRRRR), prime Edinburgh (planning restrictions), most of Cornwall (planning + price), oversupplied new-build dominated areas.

The single biggest BRRRR market mistake I see: investors basing their deal on London rental yields (3–4%) without realising those numbers don’t support the BRRRR maths. The strategy needs 6%+ gross yields to work post-refinance.

Worked example: £140k Stoke terrace, full numbers

Real numbers from a deal one of our community members closed in 2025 (sanitised). 3-bed end-of-terrace in Stoke-on-Trent, needed full refresh.

This deal recycled almost half the capital (£41k of £86k). Not perfect — a tighter buy price (£125k instead of £140k) would have pulled out 80%+. But the property is now generating ~£950/month rental income on a £45k stuck-in basis = 25% cash-on-cash yield. And the investor moved straight to deal #2 with the recycled capital.

£40k of starting capital, recycled through 5 BRRRR deals at 6 months each, builds a portfolio worth £900k+ in 3 years.

Key takeaway

A “successful” BRRRR doesn’t have to recycle 100% of capital — it just needs to work better than alternatives. £41k recycled out of £86k still beats vanilla BTL where 100% of the deposit stays trapped. Compound that across 5 deals and you have a portfolio.

7 BRRRR mistakes that cost investors their capital

I get on the phone with an investor a week who’s calling because their BRRRR deal hasn’t worked. Almost always one of these seven.

1. Buying at full market price.

If you pay 100% of post-refurb value, the maths can never work. You need to buy at 70–75% of PRV. This means you can’t usually source from Rightmove first-listings — by the time it’s on Rightmove the market has set a competitive price.

2. Underestimating refurb costs by 30%+.

First-time investors quote a contractor £20k for a refurb, then find out at week 8 that the job is actually £30k due to surprises behind the walls. Add 15–20% contingency to every refurb budget. If you can’t afford the worst case, walk.

3. Optimistic post-refurb valuation.

Investor models PRV at £200k based on one nearby comp. Lender’s RICS valuer comes in at £180k because they used 3 different comps. Refinance pulls 15% less than expected. Always model PRV using the most conservative of 3 comps, not the most flattering.

4. Refurb timeline overruns into bridge end-date.

Bridging loans have hard end-dates. If the refurb takes 9 months when you budgeted 6, you’re paying ERCs and emergency extension fees. Worst case: bridge defaults. Build a 30% time buffer into refurb schedules and have an extension plan ready.

5. Ignoring rental coverage on refinance.

Lender won’t approve a 75% LTV mortgage if the rent doesn’t cover ICR (typically 145% of mortgage interest at notional rate). Investor pulls down £150k mortgage, lender only approves £130k because rent is borderline. £20k stays trapped. Stress-test the rental side before you exchange.

6. Over-improving for the area.

A £15k designer kitchen in a £140k Stoke terrace is wasted money. The valuer caps PRV at the local ceiling regardless of finishes. Spec to area, not to your taste. Premium finishes only earn back in premium areas.

7. Skipping Article 4 / planning checks when the property will be HMO.

If your BRRRR exit is a 5-bed HMO and the area has Article 4 in force, you can’t get planning permission and the rental income falls back to family-let yields. Always check Article 4 status before you exchange. My Article 4 directions guide lists every council with restrictions.

BRRRR deal scorecard — score before you offer

Run any potential BRRRR deal through this scorecard before offering. 8+ points = good deal. 6-7 = marginal, double-check numbers. Below 6 = walk away.

+2 points

Confirmed via 3 RICS-grade comparables on the same street, last 6 months.

+2 points

Quote from at least 2 contractors, plus 15% contingency.

+2 points

At 75% LTV term mortgage at notional 5.5% stress rate. Confirms full capital recycling possible.

+1 point

Properties of this spec on the street rent within 4 weeks. Voids historically <5%.

+1 point

Confirmed via council planning portal. If HMO exit, area not at concentration threshold.

+1 point

Pulled and read by your solicitor before offering. No prohibition on letting / SA / sub-letting.

+1 point

Confirmed via specialist broker. Avoids 6-month bridge interest hold.

+1 point

If refurb runs over or valuation comes in low, you can absorb without defaulting on the bridge.

Tax: Section 24, Ltd Co, allowable expenses

BRRRR property income is taxed as standard rental income. The structural tax decisions matter most.

Personal name vs Limited Company. Section 24 mortgage interest restrictions apply to BTL properties owned personally — higher-rate taxpayers get only a 20% basic-rate credit on mortgage interest. For Ltd Co properties, mortgage interest is fully deductible against rental income. For investors aggressively scaling via BRRRR, Ltd Co (typically an SPV) is now the default. The slightly higher mortgage rates (0.2–0.4%) and accountancy costs are easily outweighed by the tax saving.

Refurb costs — capital or revenue. Most BRRRR refurb costs are capital (improving the property) and reduce CGT on eventual sale. Pure repair costs are revenue and offset rental income. The line is fuzzy and worth getting an accountant’s view on.

Stamp duty surcharge. The 3% additional rate applies to all BTL purchases. Plus a further 2% if you’re not UK-resident. Factor in stamp duty when modelling each deal — £4–8k on a typical £140–£200k purchase.

VAT on refurb. Some major refurbs (full empty-property renovations of 2+ year empty homes) qualify for 5% reduced VAT instead of 20%. Worth checking with HMRC’s VAT Notice 708 on gov.uk before paying contractors.

People also ask

What is the 2% rule for refinancing?

The 2% rule is an American concept — refinance when interest rates have dropped at least 2% below your current rate. It doesn’t translate well to the UK, where mortgage products are mostly 2- or 5-year fixes rather than 30-year fixed terms. In the UK, the trigger is your fix expiring or a forced refinance to release equity. The relevant question for BRRRR is: does the new mortgage’s rate, fees, and LTV release enough capital to make moving lender worthwhile? I’d accept a slightly higher rate to pull more equity if the deal numbers still work.

What is the 2% rule for renting?

The 2% rule (American origin) says monthly rent should be 2% of the purchase price — so a £100,000 property should rent at £2,000/month. In the UK that’s almost impossible outside a few northern HMO markets — typical UK gross yields are 0.4-0.7% per month (5-8% annually). A more useful UK rule: target a gross yield of at least 7% on a refurb-to-rent deal so that after costs, voids, and finance, the property still cashflows positively. For HMO investments, I want to see 12%+ gross yield to justify the additional management.

How does buy rent refinance work?

The strategy I teach is Buy, Refurbish, Refinance, Rent (BRRRR). You buy below market value (often using bridging or cash), refurbish to add value and meet rental standards, refinance onto a long-term BTL mortgage at the higher post-refurb valuation, and rent out for monthly cashflow. Done well, you pull most or all of your initial capital back out and own a cashflowing asset with little or no equity tied up. The key levers are buying right (10-20% below market), controlling refurb costs, and getting an accurate post-refurb valuation.

What is the 80/20 rule in refinancing?

In UK BRRRR, the 80/20 reference is usually about refinance LTV: most BTL lenders cap at 75-80% LTV after refurb. To pull all your money out, you need the post-refurb valuation × 0.75 to equal or exceed your purchase + refurb + costs. So if you buy at £80,000, spend £20,000 refurbing, and the property revalues at £140,000, you can refinance at 75% LTV (£105,000) and release £5,000 above your £100,000 input — money out, asset retained. Some specialist lenders go to 80% LTV but expect a 0.5-1% rate premium.

Frequently asked questions

How much capital do I need to start BRRRR?

Realistically £40k as a minimum for a single £100–140k BRRRR deal. That covers 25% deposit on bridging (~£25–35k), stamp duty surcharge (£3–5k), refurb cash flow (£10–25k pre-refinance), bridging interest (~£5k), legal fees (£1.5k). With £60k+ you have margin for cost overruns. With less than £30k you’re cutting too close.

How long does a typical BRRRR cycle take?

5–7 months from buy to fully tenanted with cash recycled. Buy: 4–8 weeks. Refurb: 6–16 weeks. Refinance: 4–6 weeks. Tenant find: 2–6 weeks. Some deals stretch to 9–12 months when refurbs run over or refinance is delayed.

Can I do BRRRR with no cash at all?

Almost never. Joint ventures (JVs) where you bring the project management and a partner brings the capital are the workaround if you have skills but no capital — they typically split the profit 50/50. Pure no-money-down BRRRR is mostly fictional in the UK.

What’s the difference between BRR, BRRR, and BRRRR?

Same strategy, different number of letters. BRR = Buy/Refurbish/Refinance. BRRR = adds Rent. BRRRR = adds Repeat (or re-orders to put Rent before Refinance, depending on the source). The UK community most commonly uses BRR or BRRR; the Americans popularised BRRRR.

Can I BRRRR an HMO?

Yes — and HMOs often work better for BRRRR than single-lets because the rental income is higher (improves ICR coverage), so you can pull more capital out. Watch for Article 4 directions in the area though — they require full planning permission for HMO use, which can scupper an HMO exit.

What’s the 6-month rule?

Most mainstream BTL lenders won’t refinance based on a new (post-refurb) valuation until you’ve owned the property for 6 months. Specialist lenders (Foundation, Kent Reliance, Precise) offer day-one remortgage products that ignore the 6-month rule. Crucial for BRRRR — without day-one remortgage you’re stuck on bridging for 6+ months which adds £10k+ in interest.

Should I use bridging or a refurb-to-let mortgage?

Bridging is faster (4–6 weeks) but more expensive (~1% per month). Refurb-to-let mortgages (Foundation, Kent Reliance, Precise) are slower (8–12 weeks) but cheaper. If the property needs more than 4–6 weeks of work, bridging is usually the right answer. For lighter refresh deals, refurb-to-let can save you the bridge-to-term refinance cycle.

Do BRRRR mortgages need a higher deposit than standard BTL?

The deposit on the term mortgage at refinance is the same — typically 25%. The bridging loan deposit at the buy stage is also 25%, and you may need additional cash for the refurb (which the bridge usually doesn’t cover unless you’re using a “refurb-bridge” product).

Can I BRRRR a house I already own?

Yes — sometimes called a “delayed BRRRR” or “BRRRR remortgage”. You refurbish a property you already own and refinance to pull out equity. The maths are identical; you skip the bridging step.

What happens if the post-refurb valuation comes in low?

You either accept a smaller refinance loan and leave more capital in the deal, or appeal the valuation with additional comparable evidence. Sometimes you wait 3–6 months for the local market to catch up to your spec. Worst case, you can’t pull out enough to repay the bridging — that’s when investors get into trouble.

BRRRR glossary

- PRV (Post-Refurb Value)

- The market value of the property after the refurb is complete. The single most important number in BRRRR underwriting. You buy at 70–75% of this and refinance at 75% of this.

- Bridging loan

- Short-term (3–18 month) finance at 0.65–1% per month, used to buy properties that won’t qualify for term mortgages because they need work.

- Day-one remortgage

- A specialist BTL product that lets you refinance immediately at the new post-refurb value without waiting 6 months. Foundation, Kent Reliance, Precise offer these.

- 6-month rule

- Mainstream BTL lender policy: refinance based on the new (post-refurb) valuation only after 6 months of ownership. Day-one remortgage products bypass this.

- ICR (Interest Cover Ratio)

- The lender’s stress test on rental income vs mortgage interest. Typically 145% at notional stress rate. Determines maximum loan you can get on refinance.

- SPV (Special Purpose Vehicle)

- A limited company set up to hold property investments. The default ownership structure for serious BRRRR investors due to Section 24 tax avoidance.

- Section 24

- 2017 tax change restricting mortgage interest deductibility for individual landlords (basic-rate credit only for higher-rate taxpayers). Doesn’t apply to Ltd Cos.

- Cash-on-cash yield

- Annual rental cashflow divided by cash actually left in the deal. Not gross yield. The number that matters for BRRRR — well-recycled deals can hit 25–40% cash-on-cash.

- Refurb-to-let

- A specialist BTL mortgage product that finances both the purchase and the refurb in one product. Skips the bridge-to-term refinance step.

- JV (Joint Venture)

- A partnership where one party brings capital, the other brings deal-finding and project-management skills. Profit typically split 50/50. Common in BRRRR for capital-light investors.

Want the full BRRRR + property investing playbook?

BRRRR is one of four core strategies the Property Accelerator covers — alongside HMOs, serviced accommodation, and lease options. The full system James has built over 25 years in UK property, including all the templates, contractor checklists, and lender contact lists.

James Nicholson

Founder of Property Accelerator and a UK property investor since 1999. James has built and run a personal portfolio of HMOs, BRRRR conversions and serviced accommodation across the UK, and now teaches the strategies he uses every day to thousands of UK landlords.

Related Property Accelerator guide: Picking the right city dramatically affects rental yield. Our highest yielding UK BTL areas guide ranks UK cities by gross rental yield with real 2026 figures.

About the author — James Nicholson

Founder, Property Accelerator · 25+ years investing in UK property

James has built and run portfolios across buy-to-let, HMOs, serviced accommodation, BRRRR projects and lease options. He trains thousands of UK landlords and investors through Property Accelerator and writes practical, real-world investment guides covering strategy, finance, tax and regulation.

Download NOW

4 Simple Steps To Becoming Wealthy Through Property