Inflation in the UK has reached its lowest level in two and a half years, primarily attributed to a deceleration in the rate of food price hikes. According to recent official figures, prices climbed by 3.2% over the twelve months leading up to March, marking a slight dip from the preceding month’s 3.4% increase.

This decline in inflationary pressures can be largely attributed to various factors, notably a moderation in the prices of certain consumer goods. Among the items experiencing a reduction in cost are meat, crumpets, chocolate biscuits, as well as furniture and household items. These price adjustments have contributed to the overall easing of inflationary trends across the country.

Conversely, the transportation sector has witnessed an opposing trend, with prices for petrol and diesel on the rise. This increase in fuel costs has served as a counterbalance to the downward pressure exerted by declining prices in other sectors. Despite the fluctuations observed in specific categories, the overall inflation rate remains at a relatively subdued level compared to recent years, providing a mixed outlook for consumers and policymakers alike.

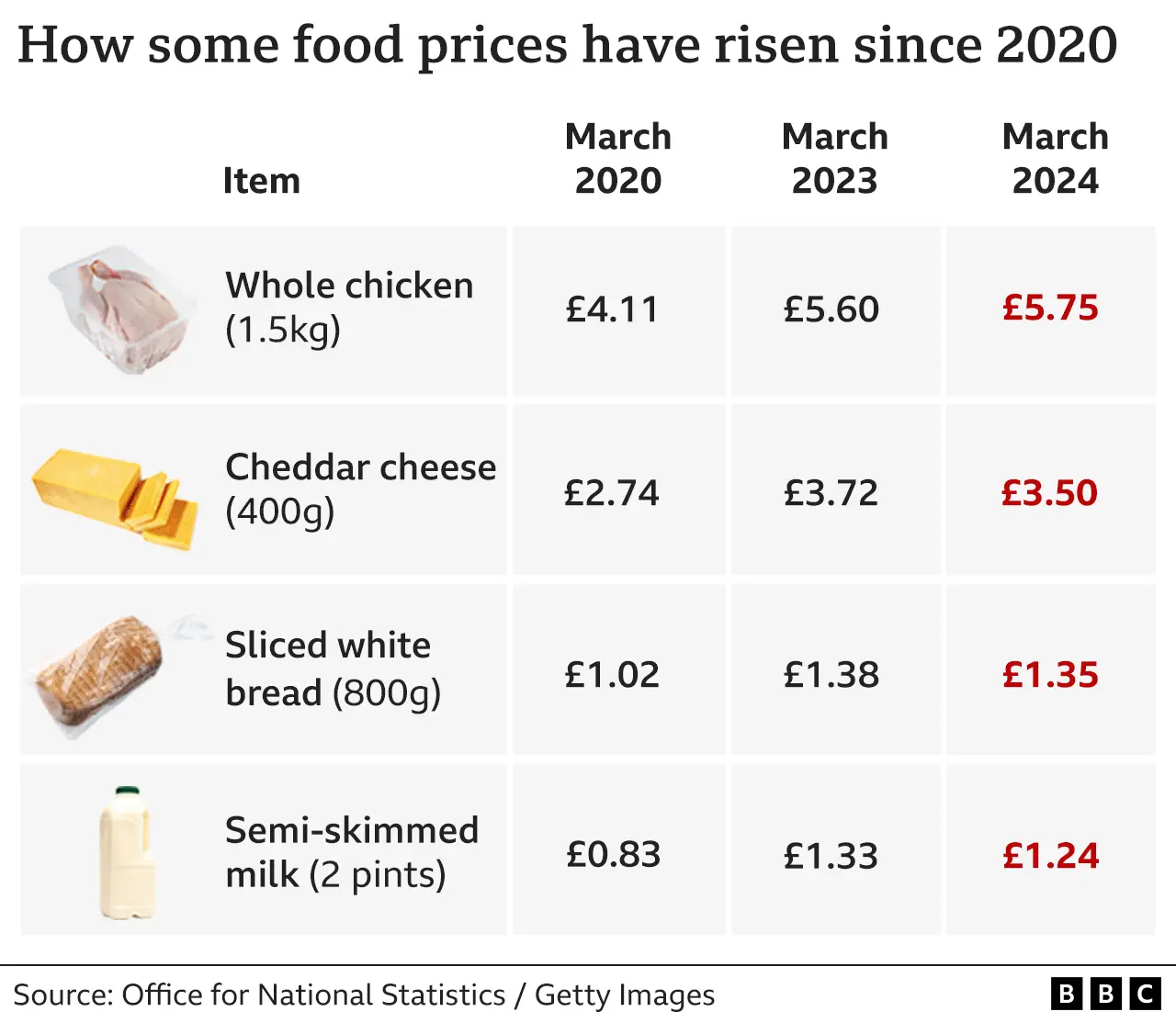

Lower inflation doesn’t necessarily translate to reduced prices; rather, it indicates a slowdown in the rate at which prices are increasing. Despite the drop in the overall inflation rate, the cost of goods available in stores still maintains a significant increase compared to prices from two years ago.

This moderation in inflationary pressures might provide a temporary respite for consumers, but it doesn’t necessarily signal a sustained trend towards cheaper goods. As economic factors continue to fluctuate, it’s essential for consumers to remain vigilant and adapt their spending habits accordingly to navigate the evolving cost landscape effectively.

The price of meat, particularly pork, experienced a notable decline of 0.5% from February to March, contrasting with a 1.4% increase recorded a year earlier. This moderation led to a slower pace of meat price growth, standing at 3.1% for the year ending in March, marking the lowest rate since November 2021.

Additionally, prices for furniture and household goods, including cleaning products, saw a decrease of 0.9% in the year leading up to March. Despite these declines, the overarching factors contributing to the UK’s persistently high inflation have primarily been attributed to surging food and energy costs in recent times.

Inflation has shown a steady decline since reaching its peak at 11.1% in late 2022, primarily influenced by the aftermath of the Covid-19 pandemic. The surge in demand for goods following the pandemic’s disruption to supply chains strained factory capacities, contributing to inflationary pressures.

Moreover, the increased demand for oil and gas post-pandemic, coupled with the geopolitical tensions stemming from Russia’s invasion of Ukraine, resulted in a further surge in prices. The conflict disrupted global supplies, exacerbating inflationary pressures. Additionally, the reduction in grain availability due to the conflict contributed to soaring food prices.

Consequently, inflation in the food and non-alcoholic drinks sector surged to nearly 20% last year, marking its highest level since the 1970s. These inflationary challenges highlight the complex interplay of global events and economic factors influencing price dynamics and consumer affordability.

In March, inflation rates exceeded economists’ predictions slightly, yet analysts suggest this is unlikely to alter expectations of potential interest rate cuts by the Bank of England, possibly commencing in June.

Yael Selfin, KPMG UK’s chief economist, anticipates inflation to revert to the 2% target later this spring, paving the way for potential interest rate reductions starting from June onwards.

Chancellor Jeremy Hunt welcomed the latest official figures, describing them as “welcome news.”

He noted that with lower inflation and the recent reduction in National Insurance by the government, effective from 6 April, individuals should begin to experience and witness the difference in their pay packets.

However, Rachel Reeves, Labour’s shadow chancellor, expressed concerns that despite these changes, working individuals would still perceive a decline in their financial situation.

“Despite these measures, prices remain elevated in stores, monthly mortgage payments are on the rise, and inflation continues to surpass the Bank of England’s target,” she remarked.

Sarah Olney, the Liberal Democrat Treasury spokesperson, echoed similar sentiments, stating, “The impact won’t be noticeable in people’s wallets. Rishi Sunak and Jeremy Hunt’s self-congratulatory tone underscores their disconnect from reality.”

The Bank is slated to announce its next interest rate decision on 9 May. With interest rates currently at their highest level in 16 years, the central bank has been steadily increasing them to mitigate inflationary pressures.

The idea behind increasing borrowing costs is to curb spending and encourage saving, thereby reducing demand for goods and helping to alleviate inflationary pressures.

In the UK, the rate of price increases varies. You can assess how inflation impacts you personally using our calculator.

Bank governor Andrew Bailey recently pondered how much evidence would be required before considering interest rate cuts in the upcoming months.

Surprisingly, consumer prices surged unexpectedly in the US last month, placing the UK’s inflation rate below that of the United States for the first time since early 2022.

Some analysts suggest that this discrepancy could prompt the Bank of England to implement interest rate cuts sooner than their US counterparts.

Both central banks, including those in Europe, have raised rates in response to surging inflation in recent years. However, with inflation declining at varying rates across different economies, their approaches to interest rates may start to diverge.

Ian Stewart, chief economist at Deloitte, noted that while inflation might be receding in the UK, the Bank of England remains cautious. Despite robust wage growth and economic recovery, there’s no rush for the Bank to slash interest rates.

Meanwhile, recent data from the Office for National Statistics revealed a 9.2% surge in private rents over the past year, averaging £1,285 in England. The upcoming inflation report for April is anticipated to show a more significant decline, attributed partly to the lower energy price cap, though households may still feel the pinch from higher direct debits.

More Property Blogs HERE:

How to Reduce Tax on Rental Income

Challenges of Owning A Second Home

What insurance is needed for a buy-to-let property?

What is the difference between remortgage and refinance UK?

Buy Refurb Refinance Rent (BRRR) Explained

Section 24 Tax Guide for Airbnb Hosts

Can you make money investing in property?

Section 24 Effect on BTL Property

How do I start a property rental business in the UK?

How to add value to your rental property

Download NOW

4 Simple Steps To Becoming Wealthy Through Property